S-Corp Distributions: What Business Owners Often Misunderstand

One of the most common points of confusion for S corp owners is this: “If my business profit is already taxed on my personal return, why do I also have to think about distributions?” It is a fair question. S corporation taxation is not always intuitive, especially for owners who are used to thinking about business income and personal income as two completely separate things. The short version is this: S corp profit generally flows through to your personal tax return whether or not you take the money out of the business. Distributions are usually not taxed a second time simply because you transferred cash from the business to yourself.

But there are important exceptions and planning issues. Basis, compensation, retained earnings, and cash flow all still matter.

One of the most common points of confusion for S-Corp owners is this:

“If my business profit is already taxed on my personal return, why do I also have to think about distributions?”

It is a fair question. S-Corporation taxation is not always intuitive, especially for owners who are used to thinking about business income and personal income as two completely separate things.

The short version is this: S-Corp profit generally flows through to your personal tax return whether or not you take the money out of the business. Distributions are usually not taxed a second time simply because you transferred cash from the business to yourself.

But there are important exceptions and planning issues. Basis, compensation, retained earnings, and cash flow all still matter. This article focuses primarily on federal tax treatment. State tax rules may differ depending on where the business and owner are located.

From C-Corp Taxation to S-Corp Taxation

A regular C corporation pays tax at the corporate level. Then, if the corporation distributes profits to shareholders as dividends, those dividends may be taxed again on the shareholders’ personal returns.

That is the “double taxation” people often hear about.

An S corporation works differently. In most cases, the S-Corp itself does not pay federal income tax on its profit. Instead, the profit flows through to the owners and is reported on their personal tax returns.

That shift is one of the main reasons business owners elect S-Corp status. It can avoid the classic C-Corp double-tax structure and, when structured properly, S corporation status may reduce certain self-employment or payroll tax exposure compared with operating as a sole proprietorship or partnership. However, the benefit depends on reasonable compensation, profit level, administrative costs, and the owner’s specific facts.

What “Flow-Through” Really Means

Flow-through taxation means the business profit is passed through to the owner for tax purposes.

For example, if your S-Corp has $200,000 of profit, that profit is generally reported to you on a Schedule K-1. You then report your share of that income on your personal tax return.

This happens whether you took the full $200,000 out of the business or left some of it in the company bank account.

That is the part many owners miss. The IRS is not only looking at how much cash you transferred to yourself. It is looking at the business profit allocated to you.

So if the company has profit, you may owe tax personally even if you did not distribute all of the cash.

Distributions Are Different From Salary

S-Corp owners often receive money from the business in two main ways:

Salary is compensation paid through payroll. It is subject to payroll taxes, withholding, and W-2 reporting.

Distributions are payments of business earnings to the owner. They are generally not treated like wages, and they are not automatically subject to payroll tax.

That difference is why S-Corp planning matters. The goal is not to avoid salary entirely. In fact, owner-employees of an S-Corp generally need to pay themselves reasonable compensation for the work they perform.

The planning question is usually how to balance salary and distributions in a way that is reasonable, supportable, and aligned with the actual economics of the business.

Distributions Are Not Automatically a Second Tax

A common misunderstanding is that distributions are taxed again when they are paid out. In many cases, they are not.

If the S-Corp already passed the profit through to you, and you have enough basis, a distribution is often just a movement of cash from the business to you personally. The tax was generally tied to the profit, not the transfer of cash itself.

That said, “generally” is doing important work here.

Distributions can create tax problems if they exceed your stock basis. Basis is a running tax calculation that reflects items such as your investment in the company, income passed through to you, losses, and prior distributions.

If distributions are larger than your available basis, part of the distribution may become taxable. That is one reason S-Corp owners should not treat distributions as an afterthought.

Basis and Retained Earnings Still Matter

Leaving money in the business does not necessarily mean you avoid tax on the profit. Taking money out does not automatically mean you pay tax again. But the details matter.

Your basis determines how much you can generally take out without triggering additional tax. Retained earnings and prior C-Corp history can also matter in certain cases, especially if the business was previously taxed as a C-Corporation before becoming an S-Corporation.

This is where business owners can get surprised. The bank account may look straightforward, but the tax rules are tracking a different set of numbers. Good bookkeeping and proactive tax planning help connect those two worlds.

Reasonable Compensation Cannot Be Ignored

S-Corp owners also need to be careful with compensation.

If you work in the business, the IRS expects you to pay yourself a reasonable salary before taking large distributions. What is “reasonable” depends on the facts: your role, industry, time worked, responsibilities, and what similar services would cost in the market.

This does not need to become overly technical for most owners, but it should be addressed deliberately. A very low salary paired with large distributions can create audit risk and possible payroll tax issues.

The better approach is to set compensation thoughtfully, document the reasoning, and revisit it as the business changes.

The Bottom Line

S-Corp taxation is powerful, but it is often misunderstood.

Profit flows through to your personal return. Salary and distributions are not the same thing. Distributions are not automatically a second tax. But basis, retained earnings, and reasonable compensation can all affect the final answer.

If you own an S-Corp, tax planning should happen before the return is prepared, not after.

That is when you still have time to understand the numbers, make better decisions, and avoid surprises.

If you own an S-Corp, tax planning should happen before the return is prepared, not after. Let’s review your salary, distributions, and basis before year-end so the tax return is not the first time you see the issue. If you own an S corporation, year-end tax planning is the right time to review salary, distributions, basis, and cash flow. A proactive review can help you understand the tax impact before the return is prepared, rather than discovering the issue after year-end.

When a Solo 401(k) May Make Sense for Consultants and S Corp Owners

For many consultants, independent professionals, and small business owners, retirement planning starts with a simple question: “Am I doing enough beyond an IRA?”

If you own a business with no U.S. employees, a solo 401(k) may be worth a closer look. It can offer more contribution flexibility than a traditional IRA or Roth IRA, especially when business income is strong. But it is not automatically the right fit for every owner, and the decision should be made alongside cash flow needs, income level, entity structure, and future hiring plans.

For many consultants, independent professionals, and small business owners, retirement planning starts with a simple question: “Am I doing enough beyond an IRA?”

If you own a business with no non-owner common-law employees who are eligible to participate in the plan, other than a spouse, a solo 401(k) may be worth a closer look. It can offer more contribution flexibility than a traditional IRA or Roth IRA, especially when business income is strong. But it is not automatically the right fit for every owner, and the decision should be made alongside cash flow needs, income level, entity structure, and future hiring plans.

Who a Solo 401(k) May Fit

A solo 401(k), sometimes called an individual 401(k), is generally designed for a business owner with no eligible employees other than a spouse.

That can include:

Independent consultants

Freelancers

Professional service providers

Sole proprietors

Single-member LLC owners

S corporation owners

Partnerships where the only participants are owners and possibly spouses

The key point is that this is an owner-only retirement plan. If the business has common-law employees who meet eligibility requirements, the plan may no longer be “solo” in practice.

For an owner who has meaningful self-employment or business income and wants to save more for retirement, the solo 401(k) can be a useful retirement planning tool.

How Contributions Work Conceptually

A solo 401(k) is different from an IRA because the business owner can potentially contribute in two roles.

First, there is the employee contribution. This is the amount the owner contributes as the worker in the business. Depending on the plan design and the owner’s situation, this may be made on a pre-tax or Roth basis.

Second, there is the employer contribution. This is the amount the business contributes on behalf of the owner. The calculation depends on how the business is structured and how the owner is paid.

For example, a sole proprietor and an S corporation owner may both use solo 401(k)s, but the contribution calculations are not identical. For an S corporation shareholder-employee, retirement plan contributions generally must be based on W-2 compensation, not shareholder distributions. A sole proprietor’s net self-employment income matters. That distinction is important because the plan has to fit the actual business structure, not just the owner’s savings goal.

A solo 401(k) still has plan rules and administrative responsibilities. Contribution limits, timing rules, plan documents, and reporting requirements matter. For example, a one-participant 401(k) is generally required to file Form 5500-EZ once plan assets reach more than $250,000 at the end of the year.

Why It May Allow Higher Contributions Than an IRA

IRAs are useful, but they have relatively modest annual contribution limits compared with many employer retirement plans.

A solo 401(k) may allow a business owner to save more because it combines employee and employer contribution capacity. For owners with enough income and available cash flow, that can create a larger retirement savings opportunity than relying on an IRA alone.

It can also give the owner more planning flexibility. Depending on the plan design, a solo 401(k) may allow pre-tax contributions, Roth contributions, employer contributions, and other features that are not available in the same way through a standard IRA.

That does not mean bigger is always better. The right contribution level should still be coordinated with tax planning, working capital, household cash needs, and long-term goals.

“I Do Not Want Money Locked Up”

This is one of the most common objections to retirement plan contributions, and it is a fair one.

Business owners often need liquidity. Income can be uneven, expenses can change, and opportunities may require cash. Putting too much into a retirement plan can create stress if the owner later needs those dollars for payroll, taxes, debt service, or personal reserves.

The planning question is not simply, “How much can I contribute?” It is, “How much can I contribute without weakening the business or the household?”

A solo 401(k) should be considered as part of a broader cash plan. That may include emergency reserves, estimated tax payments, short-term business needs, and long-term retirement funding. For some owners, the right answer is to contribute aggressively. For others, it may be to start smaller and increase contributions as income becomes more predictable.

Retirement plan assets are generally intended for long-term use. Early withdrawals may be taxable and may be subject to an additional 10% tax unless an exception applies. Some 401(k) plans allow participant loans, but loans must be permitted by the plan document and are subject to specific limits and repayment rules.

What Changes If the Business Later Hires Employees

A solo 401(k) works best when the business remains owner-only. If the business later hires employees, the plan may need to change.

Once employees become eligible under retirement plan rules, the owner may need to amend the plan, expand coverage, perform testing, or consider a different retirement plan design. At that point, the plan is no longer just a simple owner-only arrangement.

This is not a reason to avoid a solo 401(k). It is a reason to plan ahead. If hiring is likely in the near future, the owner should understand how that may affect plan administration, contribution strategy, and costs.

The Bottom Line

A solo 401(k) can be a strong retirement planning option for consultants, small business owners, and S corp owners with no U.S. employees. It may allow higher savings than an IRA and provide useful flexibility for owners with meaningful business income.

But the right plan depends on more than contribution limits. It depends on income, cash needs, employees, entity structure, and long-term goals.

If you are deciding whether a solo 401(k) fits your business, AVL Advisory can help you evaluate the tradeoffs and coordinate the decision with the rest of your financial plan.

Selling a Rental at a Loss: What Landlords Need to Know Before They Sign the Listing Agreement

Not every rental sale ends up a win. Most landlords know what to do when a property appreciates, enjoy the gain, pay the taxes, and move on. But when the numbers go the other way, a lot of people make assumptions that end up costing them.

Not every rental sale ends up a win. Most landlords know what to do when a property appreciates, enjoy the gain, pay the taxes, and move on. But when the numbers go the other way, a lot of people make assumptions that end up costing them.

Here's what you actually need to know when you're selling a rental at a loss.

The Basics: How to calculate a Rental Gain or Loss

Most people calculate late the gain or loss on their property as what they sold the property for minus what they paid for it. However, the IRS uses your adjusted basis, which takes into account:

Purchase price (what you originally paid)

Plus improvements (the new roof, the HVAC, the kitchen remodel, permanent improvements, not repairs)

Minus accumulated depreciation (every dollar of depreciation you've claimed over the years)

Generally, people get tripped up over that last piece. Depreciation reduces your basis year after year, which means your taxable gain or loss looks very different from what you see on a simple purchase-vs.-sale comparison.

Why It Matters That Rental Losses Are §1231, Not Capital

When you sell a rental property at a loss, that loss generally gets classified as a §1231 loss, not a capital loss. That distinction matters more than most people realize.

Capital losses can only offset capital gains (with a limited $3,000/year deduction against ordinary income if you have leftover losses). §1231 losses, on the other hand, are treated as ordinary losses. That means they can offset W-2 income, business income, or any other ordinary income, dollar for dollar, with no annual cap.

If you're in the 32% or 37% bracket and you have a qualifying §1231 loss, you're looking at real tax savings. This is one of the few situations where losing money on a property can actually work in your favor.

The Catch: Depreciation Recapture Doesn't Go Away

Here's where it gets counterintuitive.

Even when a property sale looks like a loss on the surface, prior depreciation can create a taxable event. Specifically, unrecaptured §1250 gain, the portion of any gain attributable to depreciation previously taken or allowed to be taken, gets taxed at 25%, regardless of your regular income tax rate.

The key words being any gain. If your adjusted basis (remember: reduced by years of depreciation) ends up below your net sale proceeds, then you have a gain, even if you sold the property for less than you paid for it. That gain gets recaptured at 25%.

In other words: the property can look like a loss in your checkbook and still produce a tax bill.

A Real-World Example

Let's say you bought a rental in 2014 for $465,000. Over the years, you put $30,000 into improvements like a new roof and updated HVAC. You held the property for 12 years and took depreciation every year.

Here's how the numbers shake out:

Purchase price $465,000

Improvements $30,000

Total cost basis $495,000

Less: 12 years of depreciation (~$15,300/yr on the depreciable portion) = ($183,600)

Adjusted basis = $311,400

Now you sell for $420,000. After a 6% commission and closing costs, net proceeds come in around $395,000.

$395,000 − $311,400 = $83,600 taxable gain

You sold the property for $45,000 less than you paid for it. You'll get a 1099-S for $420,000. And you'll owe tax on over $83,000 in gain with much of it at the 25% recapture rate.

That's the number that surprises people.

The flip side is also true: if the adjusted basis ends up above your net proceeds, you have a genuine §1231 loss, and that loss is ordinary, which means it offsets other income at your marginal rate. Additionally, depreciation recapture does not come into play since a taxable gain did not occur. That can be a meaningful tax benefit in the year of sale.

What Your CPA Needs From You

Whether you're looking at a gain, a loss, or something in between, your CPA needs documentation to get this right. Before you close, pull together:

Original HUD-1 or Closing Disclosure from when you purchased the property

Invoices for every capital improvement made over the years, not repairs, but actual improvements that extended the property's useful life or added value

Records of any equipment or appliances purchased for the rental, under current bonus depreciation rules, qualifying items may have been 100% deductible in the year of purchase, which affects your basis

Prior-year depreciation schedules from your tax returns (your CPA likely has these, but it's worth confirming)

The better your records, the more accurately we can compute your adjusted basis, and the better positioned you are to plan around the tax outcome before you close.

The Bottom Line

A loss on paper isn't always a loss on the tax return. And a "win" on the sale price isn't always a win either. The tax treatment of a rental sale depends on your adjusted basis, how long you held the property, how much depreciation you've taken, and what other income you have in the year of sale.

Run the numbers before you list, not after you close.

Thinking about selling a rental in 2026? It's worth a 15-minute call before you sign the listing agreement. We can walk through the projected tax outcome and help you decide whether the timing makes sense. Schedule a call here.

Yes, Your ESPP Income Shows Up on Your W-2 (Even Though You 'Paid' for the Shares)

Every tax season, I have the same conversation with at least one client.

"Why is my ESPP on my W-2? I bought those shares."

I get it. You put in your own money. You made the choice to participate. So why is the IRS treating part of it like a paycheck?

Because in their eyes, it is.

Every tax season, I have the same conversation with at least one client.

"Why is my ESPP on my W-2? I bought those shares."

I get it. You put in your own money. You made the choice to participate. So why is the IRS treating part of it like a paycheck?

Because in their eyes, it is.

The Discount Is Compensation, Not a Deal

ESPPs typically let you buy company stock at 10–15% below market price. That feels like a perk, and it is. But the IRS doesn't see it that way. The moment you purchase those shares, they treat the discount as compensation, the same as a bonus or a raise.

Here's a simple example. Your company stock is at $100. With a 15% discount, you pay $85. That $15 difference is ordinary income. It goes on your W-2. And here's the part most people miss: it's taxable in the year you buy, not the year you sell.

You Don't Have to Sell for the Tax to Hit

Even if you hold those shares for years without touching them, that $15 discount was already taxed the day you bought them.

This also sets your cost basis at $100, not $85. The IRS already collected tax on the discount, so you won't pay it again when you eventually sell. But only if you track it correctly.

When You Sell Matters More Than You Think

This is where ESPP planning gets interesting.

Qualifying disposition — You held the shares at least two years from the offering date and at least one year from the purchase date. The discount may be taxed at long-term capital gains rates instead of ordinary income rates. That's the favorable outcome.

Disqualifying disposition — You sell before hitting both of those thresholds. The full spread at purchase is ordinary income on your W-2. Same tax hit, but without the planning around it.

The timing of your sale isn't just a financial decision, it's also a tax one. Running the numbers before you sell, especially in a high-income year, can make a real difference.

Three Things to Check Before You File

ESPPs are still one of the most underused perks in corporate America. A guaranteed 15% discount is a strong return before the market moves an inch. But the tax piece has to be right.

Here's what I always tell clients to verify:

W-2 Box 14 — This is where most employers report ESPP income. Make sure it's there and the amount matches your records.

1099-B cost basis — Your brokerage may report your purchase price ($85 in our example) as your basis, not the full $100. If you use that lower number, you'll pay tax on the discount twice. I see this mistake more than I'd like to.

Holding period dates — Know your offering date and your purchase date. That determines whether your sale qualifies or disqualifies, and the difference matters.

Once you understand the framework, this isn't complicated. But filing without checking these three things creates real risk, either you're leaving money on the table, or you're setting yourself up for an IRS notice down the road.

If you have questions about how your ESPP fits into your overall tax picture, that's exactly what we're here for. Feel free to reach out.

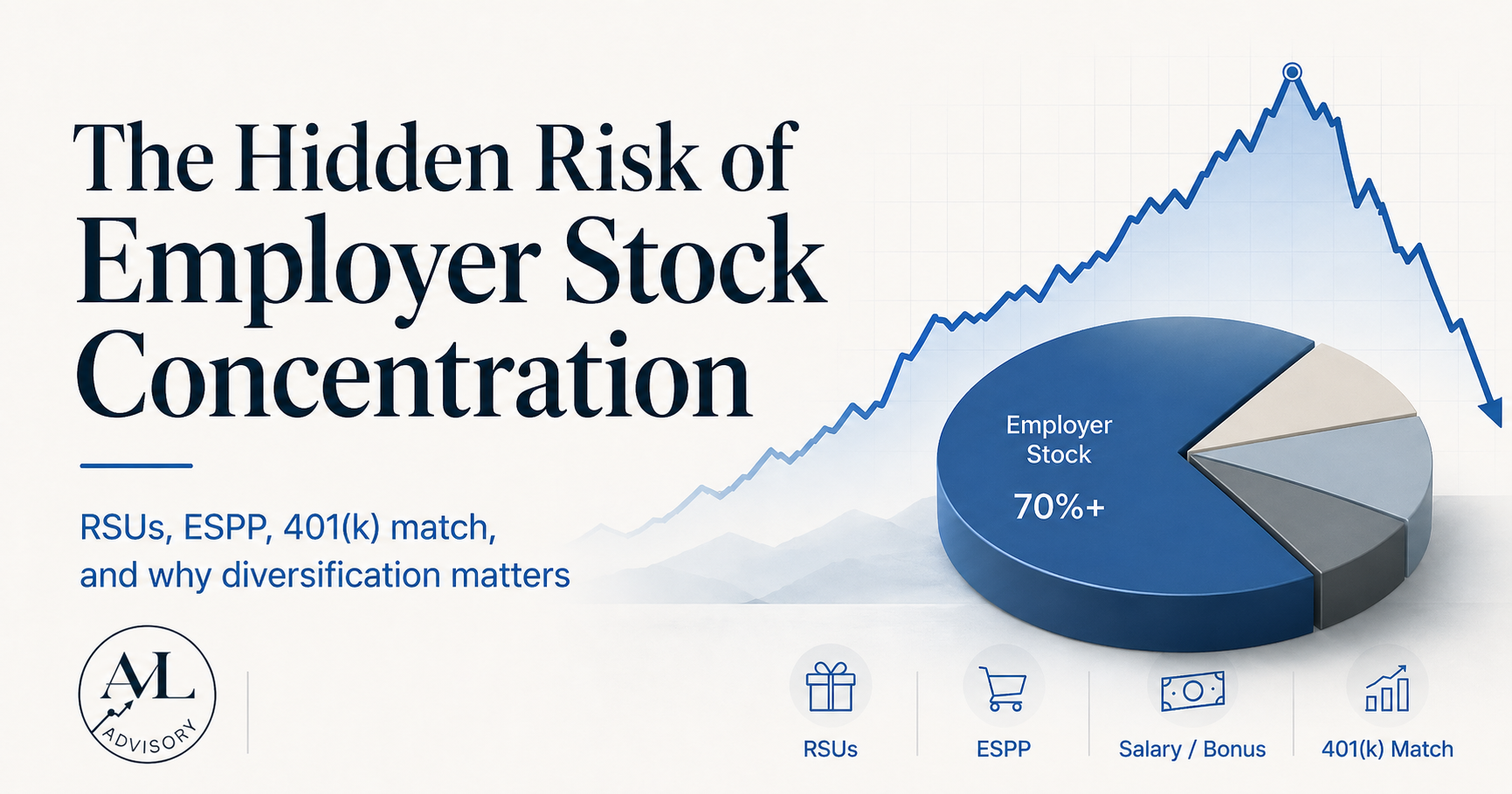

The Hidden Risk of Employer Stock Concentration: Your Paycheck and Your Portfolio Are the Same Bet

Your salary, your bonus, your RSUs, your ESPP, and your 401(k) match. If they all come from the same employer — you don't have a portfolio. You have employer concentration risk. This is the hidden financial reality for hundreds of thousands of professionals in pharma, tech, biotech, and other industries. The compensation structures that make these industries so attractive — RSUs, ESPP, generous matching — are also the structures that quietly concentrate your entire financial life into one company's stock price.

Picture this: You've spent three years watching your company's stock climb from $270 to $500. Your RSUs have vested beautifully. Your ESPP shares are sitting on a 15% discount. Your 401(k) has a healthy chunk of company match, and your upcoming bonus is tied to the same earnings call everyone's waiting on.

Then the stock slides back to $300.

Your net worth just moved on a single ticker, and you never made a decision to take that risk. It accumulated quietly, paycheck by paycheck.

This is the hidden financial reality for hundreds of thousands of professionals in pharma, tech, biotech, and other industries. The compensation structures that make these industries so attractive, RSUs, ESPP, generous matching, are also the structures that quietly concentrate your entire financial life into one company's stock price.

The Four Sources of Employer Stock Exposure

Most people think of employer stock as one thing: the shares they own. In reality, the exposure runs much deeper. There are four distinct channels through which a single employer can come to dominate your financial picture.

Salary and bonus. Your most fundamental financial asset is your human capital, your ability to earn. If your employer hits trouble, so does your income. Your emergency fund, your mortgage, your ability to invest, all of it flows from the same source.

Restricted Stock Units (RSUs). These vest over time and feel like pure upside. And they are…until they're a significant piece of your net worth. Many professionals in growth industries find that RSUs become their largest investable asset before they realize it.

Employee Stock Purchase Plans (ESPP). ESPPs offer shares at a discount, often 10-15%, with a lookback provision. The math is almost always compelling. What gets missed is that by the time the purchase period closes and shares hit your account, you may be adding fuel to a fire that's already running hot.

Employer retirement plan stock. Whether it's a 401(k) match in company shares or a pension tied to company performance, many employees have meaningful retirement exposure they don't even actively manage. It just sits there.

Taken individually, each of these is a sensible piece of compensation. Taken together, they can represent 40, 50, or even 60 percent of a household's investable assets, all in one name.

Why Even Great Companies Underperform a Diversified Portfolio

Here's the part that surprises most people: this is a risk management problem even if you believe in the company.

Think about what you're giving up when you hold a concentrated single-stock position. A diversified portfolio captures the aggregate growth of hundreds of companies. When one stumbles, others carry the weight. When your single employer stumbles, even temporarily, your entire financial position feels it.

Research from Hendrik Bessembinder at Arizona State found that over the long run, most individual stocks underperform a simple treasury bill. The broad market returns are driven by a relatively small number of exceptional winners. The problem is you don't know which ones those are in advance, and concentration in any single name raises the probability that you're on the wrong side of that distribution.

This isn't a knock on your employer. It's diversification math. And it applies to great companies as much as struggling ones.

A Sensible Diversification Glide Path

The goal isn't to sell everything at once. It's to introduce a plan that reduces concentration over time in a way that's tax-aware and psychologically manageable.

Start by identifying your lots. Every block of shares you've received has a cost basis and a holding period. Shares held more than twelve months qualify for long-term capital gains rates, meaningfully lower than short-term rates in most cases. Knowing what you own, and when you got it, is the foundation of any sensible strategy.

Layer in long-term capital gains timing. If you have shares approaching the one-year mark, it's often worth waiting to sell versus triggering a short-term gain. That said, don't let tax optimization paralyze you, a tax bill on a gain is still a good outcome. The goal is to be deliberate, not to avoid taxes at the cost of continued concentration.

Set automatic sell rules at vest. The cleanest decision is often the one you make in advance. Many employees commit to selling a portion, say, 25 to 50 percent, of each RSU tranche as it vests, before the stock has a chance to run higher (or lower) and trigger emotional second-guessing. Vesting events are natural liquidity moments. Use them.

Reinvest into a diversified structure. The proceeds don't just sit in cash. They fund the diversified portfolio that takes over the growth function your concentrated position was serving, without the single-name risk.

On the Emotional Reality of Selling

There's something that doesn't get said enough in these conversations: selling your employer's stock feels uncomfortable. It can feel like a vote of no-confidence. Like you're hedging against the team you're on. It isn't.

Selling is a risk management decision, not a loyalty decision. The people who have genuinely benefited from long careers at great companies are often the ones who regularly harvested gains along the way, not because they doubted the company, but because they had a plan for their financial life that was independent of any single outcome.

Your portfolio's job is to fund your future. That's a different job than expressing how you feel about your employer.

The Takeaway

Owning your employer's stock isn't loyalty. It's a financial decision, and like any financial decision, it deserves a plan, not a feeling.

The first step is just recognizing how much exposure you actually have. Most people are surprised when they add it up. The second step is building a framework to reduce it over time in a way that's tax-smart and doesn't require you to make a big call all at once.

If you're sitting on a meaningful position in your employer's stock, I'm happy to walk through a diversification framework that's tax-aware and built around your specific situation. Book a call with me directly, no pressure, just a conversation.

Roth IRA Conversions: When They Make Sense (and When They Don't)

A CPA breaks down the real math behind Roth IRA conversions, including the two scenarios where converting almost never makes sense and the situations where it's a no-brainer.

Roth conversions are one of those strategies that get pitched as a universal good idea. They're not. Done right, a Roth conversion can save you, or your heirs, a significant amount in lifetime taxes. Done wrong, you're writing the IRS a check today for a benefit you'll never fully realize.

Here's how to think through it clearly.

What a Roth Conversion Actually Is

A Roth conversion is the process of moving money from a traditional IRA (or other pre-tax retirement account) into a Roth IRA. The amount you convert gets added to your taxable income for the year. You pay ordinary income tax on it now, and in exchange, that money grows tax-free and comes out tax-free in retirement.

It’s a simple concept but the complexity is in the math.

When Roth Conversions Make Sense

1. You're in a Lower Tax Bracket Now Than You Expect to Be Later

This is the core logic. If you're in a 22% bracket today and expect to be in a 32% bracket in retirement, because of Social Security, RMDs, a pension, or rental income, converting now locks in the lower rate. You're essentially prepaying taxes at a discount.

This happens a lot in the years between retirement and age 73 (when required minimum distributions kick in). If you retire at 62, stop drawing a W-2, and haven't started Social Security yet, you may have a window of low taxable income. That window is prime Roth conversion territory.

2. You Have a Long Time Horizon

The tax-free compounding needs time to work. If converted funds sit in a Roth for 20–30 years, the math gets compelling fast. The shorter the runway, the harder it is to break even on the upfront tax hit.

3. You Want to Leave Tax-Free Assets to Heirs

Traditional IRAs passed to non-spouse beneficiaries must be fully distributed within 10 years under current law, and those distributions are taxable. A Roth IRA passed to heirs still has the 10-year rule, but the distributions are tax-free. For high-net-worth estates, this is a significant planning lever.

4. You Can Pay the Tax Bill from Outside the IRA

This one matters more than most people realize. If you convert $50,000 and have to pull the tax money from the IRA itself, you're reducing the amount that gets to compound tax-free. The best conversions are funded with outside money, a taxable brokerage account, savings, whatever. That way, the full converted amount stays in the Roth working for you.

5. Your State Has No Income Tax (or You're Moving to One)

If you live in Florida, Texas, Nevada, or another no-income-tax state, you're only paying federal on the conversion. If you're planning to move from a high-tax state to a no-tax state in retirement, you probably want to wait and convert after the move. Timing this right can save a meaningful amount.

When Roth Conversions Don't Make Sense

1. You're Already in a High Tax Bracket

This is probably the most common mistake. If you're in the 35% or 37% bracket today, converting a large chunk of your traditional IRA means paying top-dollar taxes right now, hoping that future rates will be even higher. That's a bet with low odds. Even if rates go up modestly, you've already paid a steep price. The math rarely works at these income levels unless you have a very specific estate planning objective.

For most people currently earning at the top brackets, the better play is to let pre-tax money stay pre-tax and focus on other tax strategies.

2. You Need the Money Soon

If you're going to need the converted funds in the next few years, you've taken the tax hit without getting the compounding benefit. Roth accounts need time. Converting in your late 60s or early 70s just to have "tax-free money" can backfire if you end up spending it down quickly anyway.

There's also the 5-year rule to be aware of: each Roth conversion has its own 5-year clock for penalty-free access to the converted principal (separate from the rule on earnings). If you're under 59½ and might need the money, this matters.

3. The Conversion Would Push You Into a Higher Bracket or Trigger Clawbacks

This is where the planning gets granular. Converting $80,000 might push your income over a threshold that:

Increases your Medicare Part B and D premiums (IRMAA surcharges)

Makes more of your Social Security taxable

Phases out certain deductions or credits

Triggers the net investment income tax

The marginal cost of the conversion in these scenarios can be much higher than the stated bracket rate. A CPA should model this before you pull the trigger, not after.

4. You're in a State With High Income Tax and Not Planning to Leave

If your state taxes ordinary income at 9–13%, converting a large IRA position is a combined federal + state hit that may never make sense unless you have a very long time horizon or significant estate planning goals. Run the numbers with both rates included.

5. You Don't Have Outside Funds to Pay the Tax

If the only way to cover the tax bill is to take it from the IRA itself, the conversion math gets much harder to justify. You're shrinking the base that needs to compound. In some cases, a smaller strategic conversion (versus a large one) is the better move.

The Bottom Line

Roth conversions aren't a blanket good idea, and they aren't a blanket bad idea. They're a tool, and like any tool, the value depends entirely on how and when you use it.

The best candidates are generally people in temporarily low-income years (between retirement and RMDs, or between jobs) who have time for the account to grow, can pay the tax from outside funds, and have a clear sense of what their future tax picture looks like.

If you don't have that clarity, that's exactly what tax planning is for.

This content is for informational purposes only and does not constitute tax or investment advice. Every situation is different — consult your CPA or financial advisor before making any conversion decisions.

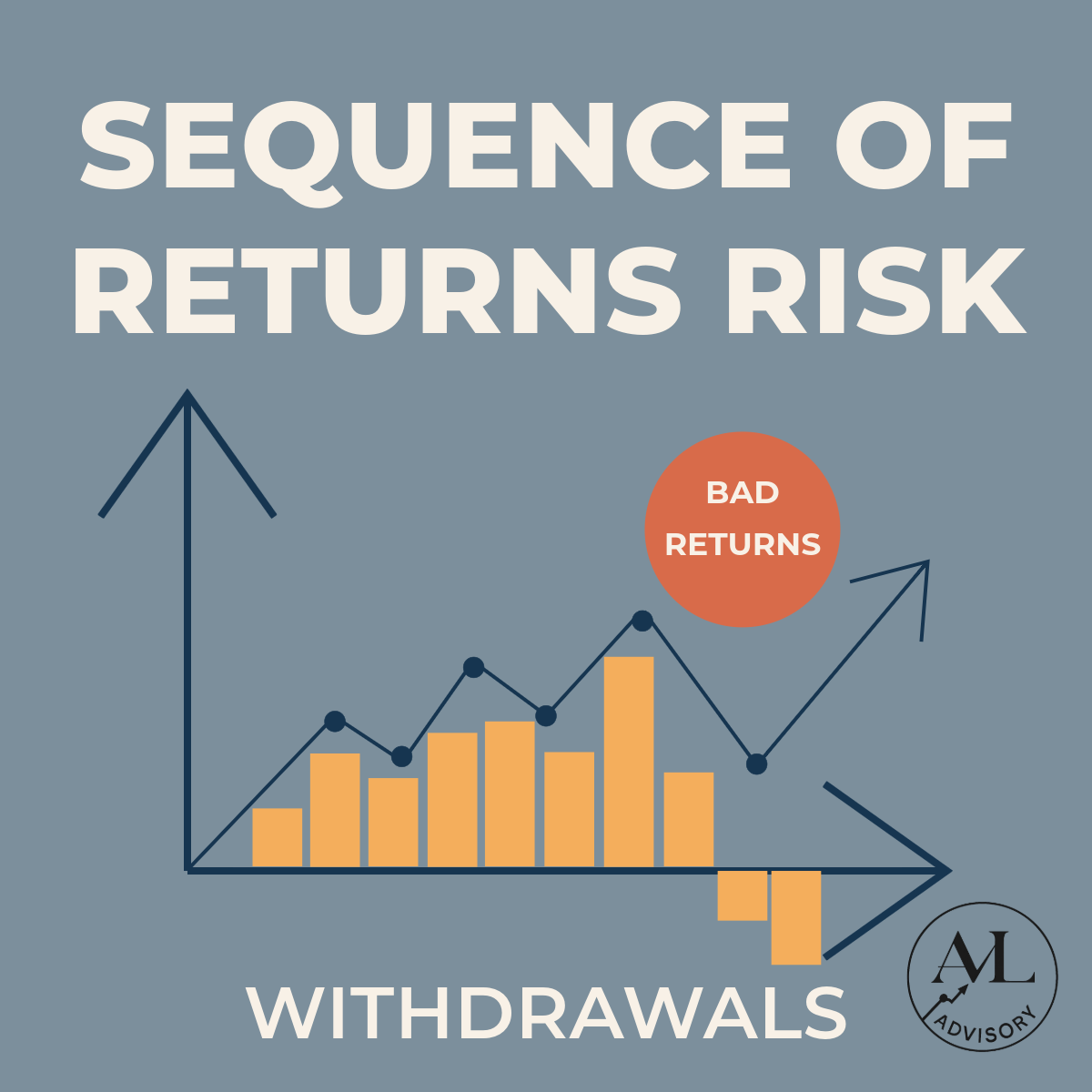

Sequence of Returns Risk: Why Timing Matters More Than You Think

Retiring in Ormond Beach or across Central Florida often means more than just “calling it a career”, it’s about designing a lifestyle around the beach, travel, family, and the freedom you’ve worked hard to earn. But that freedom depends on how long your money lasts. At AVL Advisory LLC, I help retirees and pre-retirees build tax-smart retirement income plans that can weather real-world market swings. One of the most overlooked risks in that process is something called sequence of returns risk, and understanding it can be the difference between a retirement that feels fragile and one that feels durable and confident.

Retiring in Ormond Beach or across Central Florida often means more than just “calling it a career”, it’s about designing a lifestyle around the beach, travel, family, and the freedom you’ve worked hard to earn. But that freedom depends on how long your money lasts. At AVL Advisory LLC, I help retirees and pre-retirees build tax-smart retirement income plans that can weather real-world market swings. One of the most overlooked risks in that process is something called sequence of returns risk, and understanding it can be the difference between a retirement that feels fragile and one that feels durable and confident.

When most people think about investing, they focus on average returns:

“If I earn 7% per year on average, I should be fine, right?”

The problem is that markets don’t give you a steady 7% every year. They zig and zag, some years are great, some years are painful, and many are somewhere in between.

Sequence of returns risk is the risk that those bad years show up at the wrong time, especially right before or right after you retire. And that timing can dramatically change how long your portfolio lasts, even if the average return is exactly the same.

What Is Sequence of Returns Risk?

Sequence of returns is simply the order in which you experience market gains and losses.

If markets are strong early in retirement and weaker later, your portfolio has more time to grow before you start taking big hits.

If markets drop hard in your first few retirement years, while you’re also withdrawing for income, those withdrawals can permanently shrink your nest egg and reduce its ability to recover.

The key insight:

Two retirees can earn the same average return, save the same amount, and spend the same amount, yet end up with very different outcomes, purely because of timing.

A Simple Example

Imagine two retirees:

Both start retirement with $1,000,000

Both withdraw $40,000 per year, adjusted for inflation

Both earn the same average return over 25–30 years

The only difference?

Retiree A experiences poor returns early and good returns later.

Retiree B experiences good returns early and poor returns later.

Despite identical averages, Retiree A is much more likely to run out of money first, because early losses, and withdrawals taken during those losses, dig a deeper hole that later gains may not fully fill.

That’s sequence of returns risk in action.

Why It Matters Most Near and Early in Retirement

Sequence risk is always there, but it’s especially dangerous when:

Your portfolio is at its largest

Late in your working years and early in retirement, your balances are usually the highest they’ve ever been. A 20% decline on $200,000 is very different from a 20% decline on $1,000,000.You’re taking withdrawals

During your working years, a bear market is mostly a “paper loss” if you’re still contributing. In retirement, you’re selling shares to fund your lifestyle, and selling into a down market locks in losses and leaves fewer shares to participate in the recovery.There’s less flexibility to “just work longer”

Going back to work or delaying retirement may not always be practical for health or lifestyle reasons. That makes proactive planning especially important.

How Sequence of Returns Risk Shows Up in Real Life

Here are a few real-world scenarios where timing can quietly derail a plan:

Retiring into a bear market

You retire in January, markets fall 20–30% within the first year or two, and you’re simultaneously drawing income from your portfolio.Big spending early on

You front-load retirement with major trips, home projects, or gifts during a period of poor returns. Those larger withdrawals magnify the impact of early losses.Overly aggressive allocation

You remain heavily equity-weighted into retirement without a cushion of more stable assets, making early-retirement volatility more painful.

Strategies to Manage Sequence of Returns Risk

You can’t control the market, but you can design a plan that’s more resilient to bad timing. Research and practice point to a few core strategies.

1. Spend Conservatively (Especially Early On)

Starting with a conservative, evidence-based withdrawal rate helps create a margin of safety.

Classic research (like the “4% rule”) was built around the idea of avoiding portfolio failure when early returns are poor.

More recent work suggests that dynamic, flexible withdrawals may support higher starting rates in some environments—but the principle is the same: don’t overspend early on.

A well-designed plan should stress-test different market environments, not just assume “average” returns every year.

2. Build Flexibility Into Your Spending

Static withdrawal rules (“I’ll take X% no matter what”) ignore reality. In practice, many retirees naturally adjust:

Scaling back discretionary expenses (travel, large purchases, gifts) during bear markets

Delaying big items, like a new car or kitchen remodel, if portfolios have just taken a hit

Letting withdrawals tick up in good years and down in bad years

Even modest adjustments in difficult markets can dramatically reduce the impact of sequence risk.

3. Reduce Portfolio Volatility as You Approach Retirement

Shifting from an accumulation mindset to an income and risk-management mindset is crucial. That often means:

Gradually reducing equity exposure as retirement approaches

Holding a mix of stocks, bonds, and cash instead of an all-equity portfolio

Avoiding concentration in a handful of stocks or sectors

The goal isn’t to eliminate growth, but to avoid the kind of sharp drawdowns that, combined with withdrawals, can permanently damage a plan.

4. Use “Buffer Assets” to Avoid Selling in a Crash

A very practical way to manage sequence risk is to create buckets or buffer assets you can draw from when markets are down:

Cash reserves (e.g., 6–24 months of baseline expenses)

Short-term bonds or bond ladders

Stable value or money market funds in employer plans

When stocks drop, you draw from these buffers instead of selling equities at depressed prices, giving your growth assets more time to recover.

More advanced strategies might include guaranteed income products or contingent annuities to offload some risk, but those need to be evaluated carefully within your broader plan.

5. Coordinate Taxes and Withdrawals

Sequence risk is about more than just investment returns, it’s also about how efficiently you withdraw:

Coordinating withdrawals across taxable, tax-deferred, and Roth accounts

Using market downturns as opportunities for Roth conversions

Managing capital gains and loss harvesting strategically

Thoughtful tax planning can help maintain portfolio longevity and give you more options for adjusting withdrawals without unnecessary tax drag.

When Should You Start Thinking About Sequence of Returns Risk?

It’s not just a “retiree problem.” Sequence risk becomes increasingly important when:

You’re within 5–10 years of retirement

Your retirement portfolio is becoming a major piece of your net worth

You’re counting on that portfolio for a significant portion of your future income

Planning ahead gives you time to:

Adjust your savings rate

Fine-tune your investment mix

Clarify your retirement lifestyle and spending expectations

Stress-test your plan under different market conditions

The Bottom Line

You can’t predict whether the first five years of your retirement will be smooth sailing or a stormy bear market. But you can design a plan that doesn’t break if the timing isn’t perfect.

Sequence of returns risk is really a planning problem, not a forecasting problem.

A good retirement strategy will:

Acknowledge that bad markets can show up at the worst time

Build in buffers, flexibility, and tax awareness

Adjust as life and markets change

Ready to Stress-Test Your Retirement?

Sequence of returns risk isn’t about predicting the next crash, it’s about making sure your plan can handle it. If you’re within 5–10 years of retirement (or already retired) and want to see how different market paths could affect your income, let’s run the numbers together.

I’ll help you:

Stress-test your portfolio against bad-timing scenarios

Coordinate withdrawals across taxable, IRA, and Roth accounts

Build a flexible, tax-smart income plan you can actually live with

Money Map Monday: How to Choose a Custodian (and Actually Read Your Statement)

When most people think about investing, they focus on the fun stuff: which hot stock to buy and how much it’s grown (or not). While you should also evaluate whether you are on track to meet your goals, almost no one talks about where your investments are held or how to read the statements you get every month or quarter.

That could be a problem.

Your custodian and your account statements are the plumbing of your financial life. If the plumbing isn’t solid, or you don’t understand what you’re looking at, it’s hard to design a personal wealth plan you actually trust.

This Money Map Monday is about two things:

How to choose a custodian you can feel confident about

How to read your investment statement without your eyes glazing over

When most people think about investing, they focus on the fun stuff: which hot stock to buy and how much it’s grown (or not). While you should also evaluate whether you are on track to meet your goals, almost no one talks about where your investments are held or how to read the statements you get every month or quarter.

That could be a problem.

Your custodian and your account statements are the plumbing of your financial life. If the plumbing isn’t solid, or you don’t understand what you’re looking at, it’s hard to design a personal wealth plan you actually trust.

This Money Map Monday is about two things:

How to choose a custodian you can feel confident about

How to read your investment statement without your eyes glazing over

All through the lens of my Personal Wealth Design pillar: building a coordinated, intentional plan around your goals, not just your investments.

What Is a Custodian (and Why Should You Care)?

A custodian is the company that actually holds your investment accounts and keeps your money and securities safe. Think of them as the “vault and recordkeeper” for your:

IRAs and Roth IRAs

Brokerage accounts

401(k)/403(b) rollovers

Trust and joint investment accounts

They:

Safeguard your assets

Process trades and transfers

Send you statements and tax forms

Provide online access and reporting

Your financial advisor (me, or someone like me) builds and manages your plan. Your custodian holds the accounts and keeps score.

You want both pieces working together.

Choosing a Custodian: What Actually Matters

You’ll see a lot of big brand names in this space, Fidelity, Schwab, Vanguard, etc., but the logo alone isn’t enough. Here are the key things I look at when I’m building a Personal Wealth Design for a client.

1. Safety & Protections

You want to know: What happens if something goes wrong?

Look for:

Regulation & Oversight – Is the custodian properly regulated (e.g., SEC/FINRA for broker-dealers)?

Asset Segregation – Client assets should be held separate from the firm’s own assets.

SIPC Coverage – This helps protect against the failure of the brokerage firm (not market losses). Many custodians also carry excess coverage beyond SIPC.

You can’t eliminate investment risk, but you can avoid custodians that play fast and loose with client funds.

2. Transparency of Fees

Hidden fees eat into your returns. With custodians, watch for:

Trading commissions or ticket charges

Account maintenance or inactivity fees

High internal expenses in “house brand” funds or cash products

Transfer-out or closure fees

In a well-designed plan, you should be able to see what you’re paying, to whom, and for what, advisor fees, fund expenses, and any custodian-level charges.

3. Quality of Client Experience

This is your day-to-day interaction with your money:

Is the online portal clean and easy to navigate?

Can you see performance, contributions, and withdrawals clearly?

How responsive is client service if you need help with a login, wire, or RMD form?

If it’s a headache to log in or impossible to find basic information, you’re less likely to stay engaged with your plan. Friction = avoidance.

4. Cash Management & “Sweep” Programs

Custodians love to hold your idle cash, it’s often where they make a good chunk of profit.

Look at:

What interest rate are you getting on cash?

Are there reasonable alternatives like money market funds if you want your cash to work a bit harder (while staying liquid)?

Is it clear where your cash sits and how much you have?

In a Personal Wealth Design framework, cash has a job, such as an emergency fund, near-term goals, or “dry powder” for opportunities. Your custodian should make that easy to see and manage.

5. Investment Menu & Flexibility

Most high-quality custodians will offer:

Individual stocks and bonds

ETFs and mutual funds

Certain alternatives or structured products

The question is: does the menu support your plan?

If your strategy is low-cost, globally diversified indexing, do they offer strong ETF options?

If you work with an advisor, can that advisor implement your agreed-on strategy without jumping through hoops?

The custodian should enable your design, not force you into a one-size-fits-all model.

6. Integration with Your Overall Life

A custodian works best when it integrates with:

Your tax planning (easy access to 1099s, cost basis, gain/loss reports)

Your estate plan (beneficiary designations, TODs, trust titling)

Your business interests (SEP, Solo 401(k), or business retirement plan accounts)

Personal Wealth Design is about coordination. The custodian (and your advisor) should help you see the whole picture, not create silos.

How to Read Your Investment Statement (Without Going Cross-Eyed)

Now let’s talk about the paper (or PDF) you get monthly or quarterly.

Here’s a simple framework for a 5-minute statement review that aligns with your goals.

1. Start with the Cover Summary

Most statements begin with a one-page overview. Focus on:

Beginning Value

Net Contributions/Withdrawals

Investment Gain/Loss

Ending Value

The key question:

Did my account go up because I added money, because markets went up, or both?

This matters for your mindset. If you see a big jump but it’s all contributions, that’s different from strong investment performance, and vice versa.

2. Check Your Account Titles & Beneficiaries

Make sure the account type and ownership match your plan:

Is this a Roth IRA, Traditional IRA, or Taxable Brokerage?

Is the account titled as individual, joint, or trust?

Are the beneficiaries up to date (this may show on the statement or in online settings)?

This is where Personal Wealth Design really shows up: Each account type should be chosen on purpose for tax and estate reasons, not by accident.

3. Review Holdings: What You Actually Own

You’ll see a list of securities (funds, ETFs, stocks, bonds) along with:

Quantity (how many shares you own)

Price per share

Market value

Cost basis (what you paid)

Unrealized gain/loss

Look for:

Diversification – Are you concentrated in one company, one sector, or one country?

Drift from your target allocation – Has your stock vs. bond mix wandered too far from your plan because markets moved?

The question here: Does this mix of investments still match my risk tolerance and timeline?

If your personal design calls for, say, 70% stocks / 30% bonds, and you’re now at 85% stocks after a big run-up, it may be time to rebalance (strategically, and tax-aware).

4. Look at Fees (Don’t Ignore This)

Some statements show advisor fees, trading costs, or account-level fees. These may appear in:

The activity/transactions section

A fee summary

You’re looking for:

How much was charged during the period

Who it was paid to (advisor, custodian, funds)

Whether that aligns with what you thought you were paying

Fees aren’t inherently bad, good planning and advice are worth paying for, but surprise fees are.

5. Scan the Activity Section

This is the running log of everything that happened in your account:

Contributions and deposits

Withdrawals and distributions

Dividends and interest

Trades (buys and sells)

Fees and charges

You want to confirm:

Contributions match what you planned to save

Withdrawals are intentional and fit your spending plan

No unexpected trades or transactions show up

Think of this as reviewing your “financial security camera footage.” It should be boring and predictable.

6. Tie It Back to Your Goals

A statement is just numbers unless you connect it to your Personal Wealth Design. Ask yourself:

Am I on track for my target savings rate this year?

Are these accounts aligned with specific goals (retirement, home purchase, college, early financial independence)?

Does my risk level still feel appropriate, or have life changes made it too aggressive or too conservative?

If your life has changed, career moves, marriage, kids, business growth, but your accounts haven’t, that’s a red flag.

Putting It Together: Custodian + Statement + Design

When you choose a custodian thoughtfully and actually understand your statement, something big changes:

You stop feeling intimidated by your investments

You catch issues early (fees, drift, bad account titling)

You’re able to make adjustments with confidence instead of guessing

That’s the heart of Personal Wealth Design, not just having investments, but having a coordinated system that supports your life.

A Simple Monthly Checklist

Once a month or quarter, set a 15-minute calendar reminder and run through this:

Log into your custodian’s portal

Open your most recent statement

Review:

Beginning vs. ending value

Contributions/withdrawals

Holdings and allocation

Fees and activity

Alignment with your goals

If there’s anything you don’t understand or that doesn’t look right, write it down as a question. That list becomes your agenda with your advisor or CPA/CFP.

Final Note & Disclaimer

This post is for educational purposes only and is not individualized investment advice, tax advice, or a recommendation to use any specific custodian or investment. Your situation is unique, and your choices should reflect your goals, risk tolerance, and tax picture.

If you want help:

Selecting an appropriate custodian

Designing a coordinated tax + investment strategy

Or simply having someone walk through your statement with you and translate it into plain English

That’s exactly the kind of work that falls under my Personal Wealth Design plans.

For now, your Money Map Monday action step: Pick one account, pull up the latest statement, and walk through the checklist above. Getting familiar with the plumbing is a big step toward real financial control.

Goal-Based Buckets: Give every dollar a job. Put that dollar in the right bucket. Stop guessing.

Most people mismanage their money because they juggle too many priorities at once without a clear plan. They’ve got a 401(k) over here, a checking account over there, maybe a brokerage account “for extra investing”, but no clear connection between where the dollars are sitting and what those dollars are actually for. For this week’s Money Map Monday, we’re going to fix that with a simple framework I use in my personal wealth design plans: Goal-Based Buckets.

Most people mismanage their money because they juggle too many priorities at once without a clear plan. They’ve got a 401(k) over here, a checking account over there, maybe a brokerage account “for extra investing”, but no clear connection between where the dollars are sitting and what those dollars are actually for. For this week’s Money Map Monday, we’re going to fix that with a simple framework I use in my personal wealth design plans: Goal-Based Buckets.

What Are Goal-Based Buckets?

“Goal-based buckets” is just a fancy way of saying: Organize your money by purpose and time horizon, not just by account type.

Instead of thinking in terms of “checking, savings, 401(k), Roth,” you think in terms of:

Money for now

Money for soon

Money for later

Each “bucket” has:

A clear goal

A target balance

A time horizon

An appropriate investment or savings strategy

This is personal wealth design in action: aligning your money with your financial goals, instead of letting it collect dust in random accounts.

Step 1: Get Clear on Your Big 3

Before we build buckets, we need goals.

Take five minutes and write down your top 3 financial goals over the next 1–15+ years. For example:

Build a 6-month emergency fund

Buy a home in 3–5 years

Hit work-optional or full retirement by age 60

Fund kids’ college

Start or expand a business

You don’t need every detail right now. Just a short list and rough timelines. Those timelines are what drop your goals into the right buckets.

Step 2: Build Your 3 Core Buckets

Think of this as your Money Map: three big destinations, with different rules.

Bucket 1: Now Money (0–24 Months)

This is your “now” bucket. Its job is to protect your lifestyle and keep you out of panic mode.

What goes here:

Emergency fund (typically 6-12 months of baseline expenses; more if your income is volatile)

Short-term known expenses:

Insurance premiums

Property taxes

Vacations in the next year or two

Small home or car repairs you know are coming

Typical fund vehicles:

Checking for monthly spending

High-yield savings for emergency + short-term reserves

Maybe a short-term CD or money market account

Key rule:

This bucket is not about squeezing out every last bit of return. It’s about sleep-well-at-night money. If you’re constantly dipping into long-term investments to cover short-term surprises, this bucket probably isn’t big enough or you need to adjust your budget.

Bucket 2: Soon Money (2–10 Years)

This is your flexibility bucket. It funds goals that are important but not immediate.

What goes here:

Down payment for a home in 3–5 years

Major home remodel

Starting or buying a business

Kids’ education if they’re within a decade of enrollment

Big lifestyle upgrades (boat, vacation home, extended vacay)

Typical vehicles:

Conservative to moderate investment accounts

A blend of:

Cash and short-term bonds (for stability)

Some stock exposure (for growth over multi-year periods)

Key rule:

You can’t afford to gamble here, but you also don’t want this money just sitting in cash losing purchasing power, or short-changing your goals for 5–10 years. Think measured risk to meet your goals, not all-or-nothing.

Bucket 3: Later Money (10+ Years)

This is your freedom bucket. It’s designed to support you when work becomes optional (or stops entirely).

What goes here:

Retirement accounts (401(k), 403(b), 457, IRAs)

Roth accounts

Long-term taxable investment accounts

Any assets earmarked for “future you” 10+ years down the road

Typical vehicles:

Growth-oriented investment portfolios:

Higher stock allocation

Long-term focus

Tax-smart strategies:

Using tax-deferred vs. Roth vs. taxable intentionally

Aligning investments with the tax treatment of the account

Key rule:

This is where you can accept more volatility because your time horizon is longer. The biggest mistake I see is people are not aggressive enough in their retirement accounts while they are still decades away from retirement.

Step 3: Add the “Tax Bucket” Overlay

Here’s where my CPA + advisor strategy kicks in.

On top of your time-based buckets (Now / Soon / Later), you also have tax buckets:

Taxable (brokerage, bank accounts)

Tax-deferred (traditional 401(k)/IRA, SEP, SIMPLE)

Tax-free (Roth IRA/401(k), HSA if used strategically)

A strong personal wealth design plan doesn’t just ask: “Do I have the right buckets for my goals?”

It also asks: “Are these dollars in the right type of account to manage my lifetime tax bill?”

For example:

Short-term “Now Money” usually lives in taxable accounts (you need access without penalties)

Long-term “Later Money” often leans heavily on tax-deferred and tax-free accounts

Strategic use of Roth and HSA can create powerful “future tax-free” buckets for your later years

Same goals, better tax positioning. That’s where real long-term efficiency shows up.

Step 4: Setting up your buckets

This is where most people get stuck. The idea makes sense but sometimes it doesn’t materialize because people have busy lives and may not have the time to work through the process.

Here’s a simple roadmap to implement setting up your buckets.

Name the accounts

“AVL Family Emergency Fund”

“2029 Home Down Payment”

“Lifetime Freedom Fund”

Renaming accounts in your online banking/investment platforms makes the purpose unavoidable.

2. Assign Targets

Now Bucket: “I want 6 months of expenses = $30,000”

Soon Bucket: “I want $100,000 for a down payment”

Later Bucket: “I want $X by age 60 based on my retirement plan”

3. Automate contributions

Direct deposits to checking and savings

Monthly transfers to “Soon” accounts

Percentage-of-income contributions to “Later” (401(k), IRA, etc.)

4. Set funding order

A common sequence:

Build emergency fund

Capture employer match in retirement plans

Pay off high-interest debt

Fund “Soon” goals

Increase long-term investing

You don’t need to make it perfect. You just need each dollar to know where it’s going and why.

Step 5: Your Money Map Monday Check-In

Once your buckets are set up, Money Map Monday becomes a quick review instead of a crisis meeting.

Each week (or at least once a month):

Check balances in each bucket

Confirm transfers are happening as planned

Ask:

“Does anything about my goals or time horizons need to change?”

“Is any dollar sitting in the wrong place?”

Think of it like maintaining a garden. You’re pruning, not replanting the entire thing every week.

Bringing It Back to Personal Wealth Design

Goal-Based Buckets are one of the core tools inside my personal wealth design plans because they:

Reduce anxiety (“I know where my next 6 months of expenses are coming from.”)

Improve decision-making (“I can take some risk in my Later bucket because my Now bucket is solid.”)

Create alignment (“My money, my taxes, and my timeline are finally working together.”)

If you’re a high earner juggling multiple goals and feeling like your accounts are just scattered, this is where I recommend starting.

Want Help Designing Your Buckets?

If you’d like a second set of eyes on your current setup, or you’re not sure how to align your buckets with your tax strategy and long-term plan, this is exactly what I do for clients.

We’ll:

Clarify your top goals

Map each goal to a time horizon and bucket

Layer in tax strategy so you’re not just growing wealth, you’re keeping more of it

If that sounds like the kind of structure you’ve been missing, reach out and we’ll talk about what a personal wealth design session could look like for you.

Titling Traps for Couples & Business Owners

Most couples and business owners spend more time picking paint colors or logos than they do thinking about how their accounts and assets are titled.

But “who owns what, and how” quietly controls:

What happens if you die or become disabled

Who a creditor can come after

Who actually controls an account or property

How your tax and estate planning works (or doesn’t)

In other words: titling can either support your financial plan…or accidentally blow it up.

Most couples and business owners spend more time picking paint colors or logos than they do thinking about how their accounts and assets are titled.

But “who owns what, and how” quietly controls:

What happens if you die or become disabled

Who a creditor can come after

Who actually controls an account or property

How your tax and estate planning works (or doesn’t)

In other words: titling can either support your financial plan…or accidentally blow it up.

What “titling” actually means

Titling is simply how ownership is listed on:

Bank and investment accounts

Real estate deeds

Business interests (LLC membership, S corp shares, partnership interests)

Vehicles and equipment

Beneficiary designations, POD/TOD registrations, etc.

The wording on those accounts and documents often matters just as much as what’s in your will or trust.

Titling traps for couples

Trap #1: Putting everything in one spouse’s name

I often see everything, house, retirement accounts, brokerage accounts, owned by one spouse. It usually happens because:

One spouse handles the money

One spouse earns more, or

Assets slowly migrated to the path of least resistance

Why it’s a problem:

If the “money spouse” dies or becomes disabled, the other spouse can be left navigating probate or delays just to access assets.

It can concentrate liability exposure in one person’s name.

It may not reflect what you actually want to happen if something goes wrong.

What to consider instead:

Review which assets make sense to own jointly and which should be separate.

Make sure each spouse would have access to enough liquidity if something happened to the other.

Coordinate titling with your estate plan and any state-specific rules (marital property, tenants by the entirety, etc., which vary by state).

Trap #2: Making everything joint with rights of survivorship

On the other side, some couples put everything “Joint with Right of Survivorship” (JTWROS) and assume that solves all planning issues.

Why it can backfire:

In blended families, JTWROS can unintentionally disinherit kids from a prior relationship (everything goes automatically to the survivor, regardless of the will).

Joint accounts can expose assets to the creditors or lawsuits of either joint owner.

It can undermine more nuanced estate planning using trusts.

What to consider instead:

Decide where automatic survivorship is helpful (for simplicity and probate avoidance).

For blended families or more complex situations, trusts and “Tenants in Common” structures may be better fits.

Coordinate with your estate attorney so titling lines up with your will/trust rather than working against it.

Trap #3: Relying on beneficiary designations without looking at the big picture

Retirement accounts, life insurance, and many investment accounts allow you to name primary and contingent beneficiaries. Bank and brokerage accounts may also allow “Payable on Death” (POD) or “Transfer on Death” (TOD) designations.

The trap:

Beneficiary forms are often filled out once and never updated.

People assume “my will covers it,” but beneficiary designations override your will.

Over time, people divorce, remarry, have kids, start businesses, and never circle back.

Result:

Ex-spouses still listed.

No contingent beneficiaries (assets may go to your estate and through probate).

Beneficiaries that conflict with your actual estate plan.

What to consider instead:

Review all beneficiary forms periodically, especially after major life changes (marriage, divorce, kids, business sale).

Confirm that names, percentages, and contingents match your broader plan.

Coordinate beneficiary designations with any trusts you’ve set up.

Trap #4: Adding kids or parents as co-owners “for convenience”

A very common one: adding an adult child or parent to a bank account or deed so “they can help pay bills” or “avoid probate.”

Why this can be risky:

You may be making an unintended gift for tax purposes.

Their creditors, lawsuits, or divorces might go after your asset.

When you die, that asset may pass 100% to that co-owner, cutting out other intended heirs.

What to consider instead:

Use properly drafted powers of attorney or authorized signer roles instead of ownership where appropriate.

Use beneficiary, POD/TOD, or trust structures to avoid probate without creating other problems.

Talk with an attorney and tax professional before adding anyone as a co-owner.

Titling traps for business owners

Business owners have an extra layer of complexity: personal and business titling can easily get tangled.

Trap #5: Mixing business and personal ownership

You might:

Run the business through an LLC or S-Corp…

But title real estate, vehicles, or key assets in your personal name

Or, worse, run everything in your personal name and treat it “like a business”

Why it’s a problem:

It can weaken liability protection (piercing the corporate veil).

It muddies tax treatment and makes bookkeeping a nightmare.

It complicates a future sale of the business or succession planning.

What to consider instead:

Decide which assets truly belong to the business versus you personally.

Title key business assets (equipment, IP, vehicles, etc.) consistently with your entity structure.

Keep business accounts and personal accounts clearly separated.

Trap #6: Giving a spouse or partner ownership “just in case” with no plan behind it

Sometimes a spouse or partner is added as a co-owner of the business “to help,” “for income,” or “for protection,” but there’s:

No operating agreement

No buy-sell agreement

No clarity on decision-making or what happens if you split, die, or sell

Why it can blow up:

If the relationship changes, you may have an unintended business partner with legal rights.

A death, disability, or divorce can freeze decision-making or trigger expensive disputes.

It can complicate any future sale or transition.

What to consider instead:

Be intentional about who actually owns equity vs. who’s on payroll.

Work with an attorney to put a clear operating agreement or shareholders’ agreement in place.

Use life and disability insurance, plus buy-sell provisions, to plan for “what ifs.”

Trap #7: Business real estate titled without a strategy

Common scenario: the business operates in a building you or your entity owns, but:

The property is titled in your personal name,

Or it sits in a separate LLC,

With no clear tax or asset-protection strategy driving the decision.

Potential issues:

Missed planning opportunities for rent deductions and long-term tax planning.

Asset-protection gaps if a lawsuit targets the operating business or the property.

Confusion around what actually gets sold if you sell the business.

What to consider instead:

Decide whether real estate should live in a separate entity and be leased to the operating company.

Make sure lease arrangements and titling coordinate with your tax strategy.

Think ahead: if you sold the business, would you keep the building? Titling should reflect that plan.

Trap #8: Outdated business titling after you’ve “upgraded” your entity

Many owners start as a sole proprietor, then later create an LLC or elect S-Corp status. The trap is never updating:

Bank accounts

Vendor and customer contracts

Licenses, permits, or insurance

Domain names, IP, and other intangible assets

Result:

Some things are still titled in your personal name or under the old entity.

Liability and tax treatment may not match what you think you have.

It complicates selling, valuing, or transferring the business.

What to consider instead:

When you change entity type, create a checklist to update titling across the board.

Work with your CPA and attorney to formally move assets and contracts to the new entity where appropriate.

Maintain clean records of ownership, capital contributions, and transfers.

How to clean up your titling (without losing your mind)

You don’t have to fix everything overnight. Start with a simple process:

Inventory everything

List bank accounts, investment accounts, retirement accounts, real estate, vehicles, business interests, insurance policies, etc.

Note exactly how each is titled and who the beneficiaries are.

Highlight red flags

Look for:Everything in one spouse’s name

Outdated or missing beneficiaries

Assets co-owned with kids or parents “for convenience”

Business assets titled personally (or vice versa)

Ownership that doesn’t match your will, trust, or business agreements

Prioritize the high-impact items

Anything that could cause a big tax, estate, or liability issue moves to the top of the list.

Fix those first with your advisor team.

Coordinate with your “triangle” of advisors

CPA/Tax advisor – to understand tax implications of moving assets.

Financial planner – to align titling with your goals, risk management, and investment strategy.

Estate/business attorney – to update documents, deeds, and agreements correctly.

Revisit periodically

Marriage/divorce, kids, new business, selling a business, moving states, or major windfalls are all triggers to review titling again.

Where I come in

At AVL Advisory, I look at your entire picture, taxes, investments, business, and estate planning, so we can spot titling traps before they become expensive problems.

For couples, that means:

Making sure each of you is protected and provided for

Aligning account titling with your wills, trusts, and beneficiary designations

Reducing surprises and “accidental disinheritance”

For business owners, that means:

Cleaning up how business and personal assets are held

Coordinating entity structure, titling, and tax strategy

Building a plan that supports the business you have and the exit you eventually want

If you’re not sure how your accounts and assets are titled, or you have a nagging feeling something isn’t quite right, this is exactly the type of work I help clients with.

If you’d like a coordinated review of your titling, taxes, and financial plan, you can book a call directly from my website’s contact page or online calendar.

Useful references:

Consumer Financial Protection Bureau – estate and housing guides

FDIC – how different account types are treated

Own-Occupation vs Any-Occupation Disability Insurance: What’s the Difference and Why It Matters

Own-Occ vs Any-Occ: the definition in your disability policy determines if/when you get paid. I broke down the differences, pros/cons, and what to watch for in plain English. Disability insurance replaces a portion of your income if an illness or injury prevents you from working. Policies can be short-term (often three to six months) or long-term (potentially to retirement age), and the most critical clause in any policy is its definition of disability, that wording controls when benefits get paid.

Disability insurance replaces a portion of your income if an illness or injury prevents you from working. Policies can be short-term (often three to six months) or long-term (potentially to retirement age), and the most critical clause in any policy is its definition of disability, that wording controls when benefits get paid.

Quick refresher: how disability insurance works

Long-term disability insurance is designed to replace a set percentage of your earnings, commonly in the 50–70% range, and benefits begin after a waiting (“elimination”) period. Typical features to evaluate include: the disability definition, benefit period, elimination period, residual/partial benefits, COLA riders, renewability, and potential offsets with other benefits (e.g., Social Security).

The two key definitions of disability

1) Own-Occupation

You’re considered disabled if you cannot perform the regular and customary duties of your own occupation due to a covered illness or injury. Many long-term policies start with an own-occupation definition for the first year or two of a claim (some keep it for the full benefit period). Because it’s easier to qualify under this standard, premiums are typically higher.