Sequence of Returns Risk: Why Timing Matters More Than You Think

Retiring in Ormond Beach or across Central Florida often means more than just “calling it a career”, it’s about designing a lifestyle around the beach, travel, family, and the freedom you’ve worked hard to earn. But that freedom depends on how long your money lasts. At AVL Advisory LLC, I help retirees and pre-retirees build tax-smart retirement income plans that can weather real-world market swings. One of the most overlooked risks in that process is something called sequence of returns risk, and understanding it can be the difference between a retirement that feels fragile and one that feels durable and confident.

When most people think about investing, they focus on average returns:

“If I earn 7% per year on average, I should be fine, right?”

The problem is that markets don’t give you a steady 7% every year. They zig and zag, some years are great, some years are painful, and many are somewhere in between.

Sequence of returns risk is the risk that those bad years show up at the wrong time, especially right before or right after you retire. And that timing can dramatically change how long your portfolio lasts, even if the average return is exactly the same.

What Is Sequence of Returns Risk?

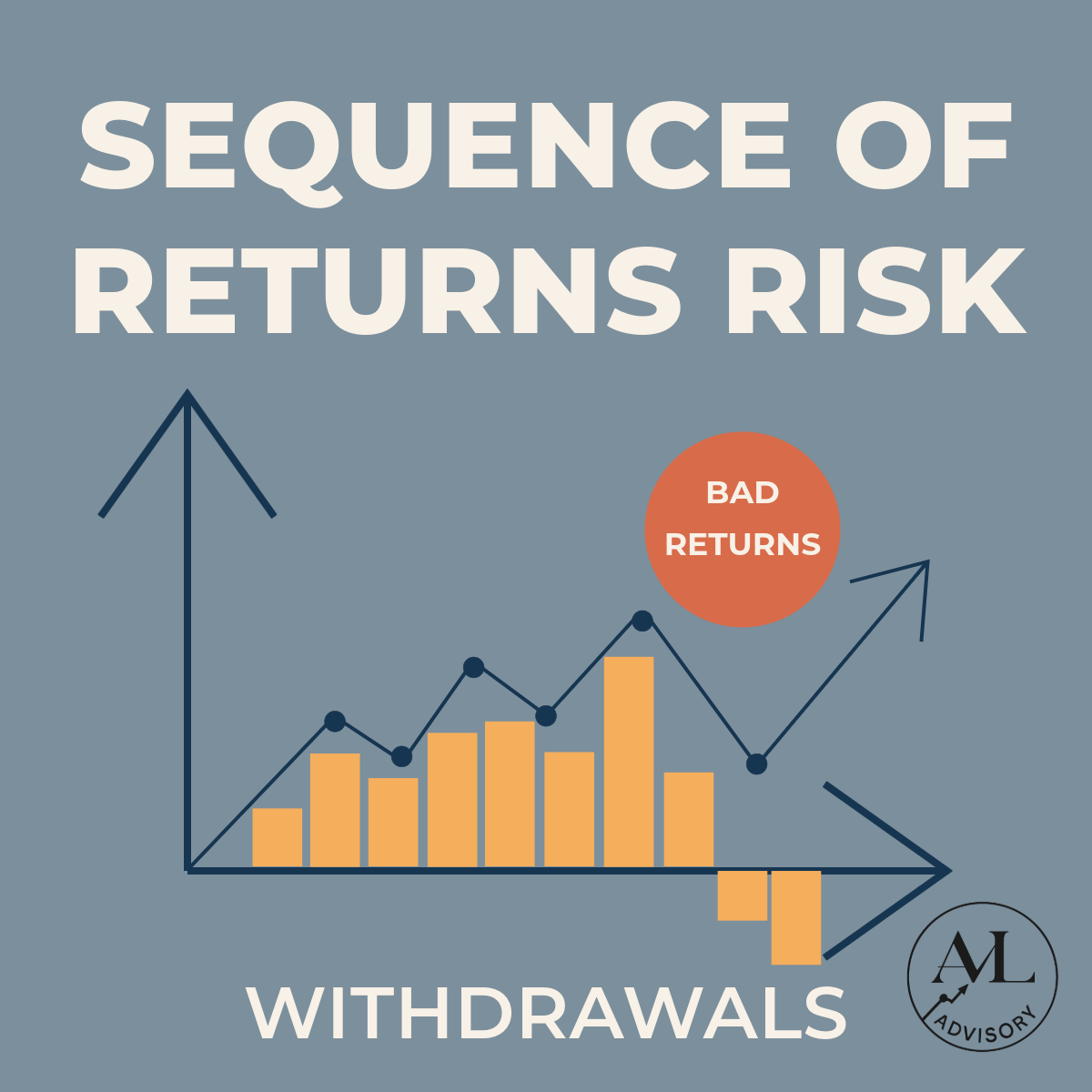

Sequence of returns is simply the order in which you experience market gains and losses.

If markets are strong early in retirement and weaker later, your portfolio has more time to grow before you start taking big hits.

If markets drop hard in your first few retirement years, while you’re also withdrawing for income, those withdrawals can permanently shrink your nest egg and reduce its ability to recover.

The key insight:

Two retirees can earn the same average return, save the same amount, and spend the same amount, yet end up with very different outcomes, purely because of timing.

A Simple Example

Imagine two retirees:

Both start retirement with $1,000,000

Both withdraw $40,000 per year, adjusted for inflation

Both earn the same average return over 25–30 years

The only difference?

Retiree A experiences poor returns early and good returns later.

Retiree B experiences good returns early and poor returns later.

Despite identical averages, Retiree A is much more likely to run out of money first, because early losses, and withdrawals taken during those losses, dig a deeper hole that later gains may not fully fill.

That’s sequence of returns risk in action.

Why It Matters Most Near and Early in Retirement

Sequence risk is always there, but it’s especially dangerous when:

Your portfolio is at its largest

Late in your working years and early in retirement, your balances are usually the highest they’ve ever been. A 20% decline on $200,000 is very different from a 20% decline on $1,000,000.You’re taking withdrawals

During your working years, a bear market is mostly a “paper loss” if you’re still contributing. In retirement, you’re selling shares to fund your lifestyle, and selling into a down market locks in losses and leaves fewer shares to participate in the recovery.There’s less flexibility to “just work longer”

Going back to work or delaying retirement may not always be practical for health or lifestyle reasons. That makes proactive planning especially important.

How Sequence of Returns Risk Shows Up in Real Life

Here are a few real-world scenarios where timing can quietly derail a plan:

Retiring into a bear market

You retire in January, markets fall 20–30% within the first year or two, and you’re simultaneously drawing income from your portfolio.Big spending early on

You front-load retirement with major trips, home projects, or gifts during a period of poor returns. Those larger withdrawals magnify the impact of early losses.Overly aggressive allocation

You remain heavily equity-weighted into retirement without a cushion of more stable assets, making early-retirement volatility more painful.

Strategies to Manage Sequence of Returns Risk

You can’t control the market, but you can design a plan that’s more resilient to bad timing. Research and practice point to a few core strategies.

1. Spend Conservatively (Especially Early On)

Starting with a conservative, evidence-based withdrawal rate helps create a margin of safety.

Classic research (like the “4% rule”) was built around the idea of avoiding portfolio failure when early returns are poor.

More recent work suggests that dynamic, flexible withdrawals may support higher starting rates in some environments—but the principle is the same: don’t overspend early on.

A well-designed plan should stress-test different market environments, not just assume “average” returns every year.

2. Build Flexibility Into Your Spending

Static withdrawal rules (“I’ll take X% no matter what”) ignore reality. In practice, many retirees naturally adjust:

Scaling back discretionary expenses (travel, large purchases, gifts) during bear markets

Delaying big items, like a new car or kitchen remodel, if portfolios have just taken a hit

Letting withdrawals tick up in good years and down in bad years

Even modest adjustments in difficult markets can dramatically reduce the impact of sequence risk.

3. Reduce Portfolio Volatility as You Approach Retirement

Shifting from an accumulation mindset to an income and risk-management mindset is crucial. That often means:

Gradually reducing equity exposure as retirement approaches

Holding a mix of stocks, bonds, and cash instead of an all-equity portfolio

Avoiding concentration in a handful of stocks or sectors

The goal isn’t to eliminate growth, but to avoid the kind of sharp drawdowns that, combined with withdrawals, can permanently damage a plan.

4. Use “Buffer Assets” to Avoid Selling in a Crash

A very practical way to manage sequence risk is to create buckets or buffer assets you can draw from when markets are down:

Cash reserves (e.g., 6–24 months of baseline expenses)

Short-term bonds or bond ladders

Stable value or money market funds in employer plans

When stocks drop, you draw from these buffers instead of selling equities at depressed prices, giving your growth assets more time to recover.

More advanced strategies might include guaranteed income products or contingent annuities to offload some risk, but those need to be evaluated carefully within your broader plan.

5. Coordinate Taxes and Withdrawals

Sequence risk is about more than just investment returns, it’s also about how efficiently you withdraw:

Coordinating withdrawals across taxable, tax-deferred, and Roth accounts

Using market downturns as opportunities for Roth conversions

Managing capital gains and loss harvesting strategically

Thoughtful tax planning can help maintain portfolio longevity and give you more options for adjusting withdrawals without unnecessary tax drag.

When Should You Start Thinking About Sequence of Returns Risk?

It’s not just a “retiree problem.” Sequence risk becomes increasingly important when:

You’re within 5–10 years of retirement

Your retirement portfolio is becoming a major piece of your net worth

You’re counting on that portfolio for a significant portion of your future income

Planning ahead gives you time to:

Adjust your savings rate

Fine-tune your investment mix

Clarify your retirement lifestyle and spending expectations

Stress-test your plan under different market conditions

The Bottom Line

You can’t predict whether the first five years of your retirement will be smooth sailing or a stormy bear market. But you can design a plan that doesn’t break if the timing isn’t perfect.

Sequence of returns risk is really a planning problem, not a forecasting problem.

A good retirement strategy will:

Acknowledge that bad markets can show up at the worst time

Build in buffers, flexibility, and tax awareness

Adjust as life and markets change

Ready to Stress-Test Your Retirement?

Sequence of returns risk isn’t about predicting the next crash, it’s about making sure your plan can handle it. If you’re within 5–10 years of retirement (or already retired) and want to see how different market paths could affect your income, let’s run the numbers together.

I’ll help you:

Stress-test your portfolio against bad-timing scenarios

Coordinate withdrawals across taxable, IRA, and Roth accounts

Build a flexible, tax-smart income plan you can actually live with