The Hidden Risk of Employer Stock Concentration: Your Paycheck and Your Portfolio Are the Same Bet

Picture this: You've spent three years watching your company's stock climb from $270 to $500. Your RSUs have vested beautifully. Your ESPP shares are sitting on a 15% discount. Your 401(k) has a healthy chunk of company match, and your upcoming bonus is tied to the same earnings call everyone's waiting on.

Then the stock slides back to $300.

Your net worth just moved on a single ticker, and you never made a decision to take that risk. It accumulated quietly, paycheck by paycheck.

This is the hidden financial reality for hundreds of thousands of professionals in pharma, tech, biotech, and other industries. The compensation structures that make these industries so attractive, RSUs, ESPP, generous matching, are also the structures that quietly concentrate your entire financial life into one company's stock price.

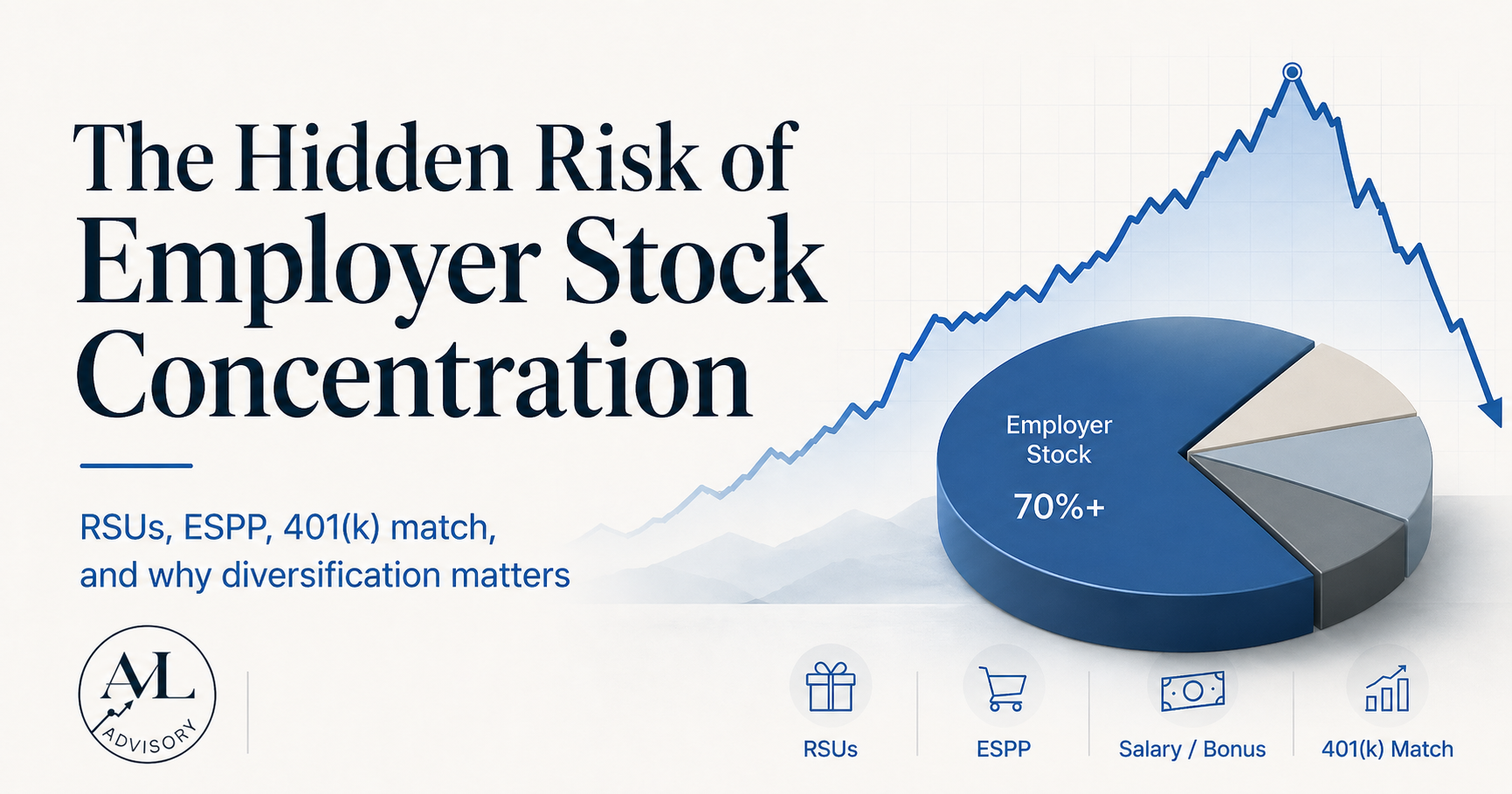

The Four Sources of Employer Stock Exposure

Most people think of employer stock as one thing: the shares they own. In reality, the exposure runs much deeper. There are four distinct channels through which a single employer can come to dominate your financial picture.

Salary and bonus. Your most fundamental financial asset is your human capital, your ability to earn. If your employer hits trouble, so does your income. Your emergency fund, your mortgage, your ability to invest, all of it flows from the same source.

Restricted Stock Units (RSUs). These vest over time and feel like pure upside. And they are…until they're a significant piece of your net worth. Many professionals in growth industries find that RSUs become their largest investable asset before they realize it.

Employee Stock Purchase Plans (ESPP). ESPPs offer shares at a discount, often 10-15%, with a lookback provision. The math is almost always compelling. What gets missed is that by the time the purchase period closes and shares hit your account, you may be adding fuel to a fire that's already running hot.

Employer retirement plan stock. Whether it's a 401(k) match in company shares or a pension tied to company performance, many employees have meaningful retirement exposure they don't even actively manage. It just sits there.

Taken individually, each of these is a sensible piece of compensation. Taken together, they can represent 40, 50, or even 60 percent of a household's investable assets, all in one name.

Why Even Great Companies Underperform a Diversified Portfolio

Here's the part that surprises most people: this is a risk management problem even if you believe in the company.

Think about what you're giving up when you hold a concentrated single-stock position. A diversified portfolio captures the aggregate growth of hundreds of companies. When one stumbles, others carry the weight. When your single employer stumbles, even temporarily, your entire financial position feels it.

Research from Hendrik Bessembinder at Arizona State found that over the long run, most individual stocks underperform a simple treasury bill. The broad market returns are driven by a relatively small number of exceptional winners. The problem is you don't know which ones those are in advance, and concentration in any single name raises the probability that you're on the wrong side of that distribution.

This isn't a knock on your employer. It's diversification math. And it applies to great companies as much as struggling ones.

A Sensible Diversification Glide Path

The goal isn't to sell everything at once. It's to introduce a plan that reduces concentration over time in a way that's tax-aware and psychologically manageable.

Start by identifying your lots. Every block of shares you've received has a cost basis and a holding period. Shares held more than twelve months qualify for long-term capital gains rates, meaningfully lower than short-term rates in most cases. Knowing what you own, and when you got it, is the foundation of any sensible strategy.

Layer in long-term capital gains timing. If you have shares approaching the one-year mark, it's often worth waiting to sell versus triggering a short-term gain. That said, don't let tax optimization paralyze you, a tax bill on a gain is still a good outcome. The goal is to be deliberate, not to avoid taxes at the cost of continued concentration.

Set automatic sell rules at vest. The cleanest decision is often the one you make in advance. Many employees commit to selling a portion, say, 25 to 50 percent, of each RSU tranche as it vests, before the stock has a chance to run higher (or lower) and trigger emotional second-guessing. Vesting events are natural liquidity moments. Use them.

Reinvest into a diversified structure. The proceeds don't just sit in cash. They fund the diversified portfolio that takes over the growth function your concentrated position was serving, without the single-name risk.

On the Emotional Reality of Selling

There's something that doesn't get said enough in these conversations: selling your employer's stock feels uncomfortable. It can feel like a vote of no-confidence. Like you're hedging against the team you're on. It isn't.

Selling is a risk management decision, not a loyalty decision. The people who have genuinely benefited from long careers at great companies are often the ones who regularly harvested gains along the way, not because they doubted the company, but because they had a plan for their financial life that was independent of any single outcome.

Your portfolio's job is to fund your future. That's a different job than expressing how you feel about your employer.

The Takeaway

Owning your employer's stock isn't loyalty. It's a financial decision, and like any financial decision, it deserves a plan, not a feeling.

The first step is just recognizing how much exposure you actually have. Most people are surprised when they add it up. The second step is building a framework to reduce it over time in a way that's tax-smart and doesn't require you to make a big call all at once.

If you're sitting on a meaningful position in your employer's stock, I'm happy to walk through a diversification framework that's tax-aware and built around your specific situation. Book a call with me directly, no pressure, just a conversation.